X

Trustworthy Source

U.S. Securities and Exchange Commission

Independent U.S. government agency responsible for regulating the securities industry, which includes stocks and options exchanges

Go to source

Negotiating Lower Fees

Calculate your total fees. You can find data on the fees you're being charged in a number of ways, but the simplest and most straightforward way is to review the account statements you receive and make a projection. Generally, you'll see two kinds of fees on your statements. Some will be transaction fees, which are only charged when you buy or sell a stock or mutual fund. Others are ongoing fees, such as account maintenance fees or management fees, which you are charged on a regular basis. Both types of fees reduce the value of your investment. Ongoing fees can have a significant impact over time, particularly if you have a low rate of return on your investments. Ongoing fees typically are expressed as a percentage of your investment portfolio, which means as your investment increases, the fees will increase as well.

Ask questions about your fees. If you don't understand any of the fees that you're being charged, your broker should be able to explain them to you more thoroughly. You need to know exactly what the fee is and why you were charged it. Even though your account statements are the easiest way to learn about your fees, those statements may include jargon or abbreviations that isn't clear. This is especially true if you are new to investing. When you ask your broker about the fees, make sure they communicate to you in a way you'll understand. You can try the "explain it to me like I'm six years old" approach to ensure your broker will tell you the information you need without using a lot of confusing terminology or industry jargon.

Identify which fees can be lowered. Once you've figured out exactly what fees you're being charged and why, you can isolate the ones that you can try to negotiate down. Three types of fees typically can be negotiated down: management fees, transaction fees, and commissions. Your management fee is a percentage of your total investment, which means as your investment grows, the fee also will get larger. A percentage that seems low when you're just starting out can cause you to lose a lot of money in the long run, so it's in your best interests to get this rate as low as possible, as soon as possible. Transaction fees typically are pretty low, and if you don't make a lot of trades they shouldn't be a big concern. However, if you're buying and selling left and right, these fees can add up. In that situation, it makes sense to try to negotiate a lower rate. If you've invested in (or want to invest in) a mutual fund that is front-end loaded, you'll be paying a commission (or "load") up front when you open your account. You can always choose a no-load fund to avoid this cost entirely, but if you can't find one that suits your needs, you can at least try to negotiate this fee down.

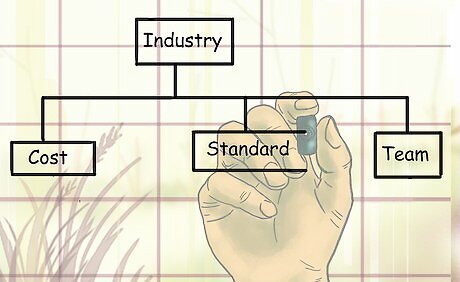

Determine an industry standard. It's rare for people not professionally involved in the finance sector to have much of an idea how much they should be paying for investment services. You must equip yourself with this information before you attempt to negotiate for lower investment fees. Management fees, retainers, and hourly rates vary dramatically in the finance industry, so you'll have to do some research to figure out how the fees you're being charged stack up to what others charge. Keep in mind that the amount you pay for someone else to manage your investments depends on how much work that person does and how much you're willing (and able) to do yourself. If you don't mind educating yourself on the way the market works, you can potentially do much of the work your broker does for you, which gives you room to negotiate even lower rates. When you're looking at fees for different brokerage firms, only compare your current broker's fees with those charged by similar brokers at brokerage firms of a similar size and age. This gives you a more reasonable basis of comparison.

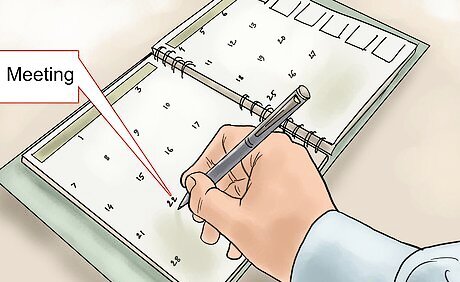

Schedule a meeting with your financial professional. If you want to negotiate for lower fees, it's important to have a conversation with your broker or advisor directly in person. Set the meeting far enough out that you have time to get together the materials you need. When you go into the meeting, it's important that you are knowledgeable, both about the fees you're being charged and about the industry standard. If you found articles or other material through your research that supports your argument for lower fees, bring it along so your broker can review it and better understand where you're coming from. You also should bring a tablet or some paper and a pen so that you can take notes during the negotiation. If you and your broker reach an agreement, you'll want to follow up in writing to confirm the agreement so you have a record.

Request lower fees. When you sit down with your broker or financial advisor, let them know up front the purpose for your meeting. If they are absolutely unwilling to negotiate your fees, you'll save yourself a lot of time and effort. Be confident, certain, and knowledgeable when you ask your broker to lower your investment fees. You've done your homework, and you know that you're paying higher fees than you should. In some cases, your broker won't have any trouble giving you a reduced rate – it's just a matter of asking. In others, your broker may be angry or insulted that you would try to get their services more cheaply. Keep in mind that your relationship with your financial advisor is just like any other relationship. When you come in to ask for lower fees, there's a chance your advisor may take it personally, or think you are unhappy with them. Make it clear that this isn't the case.

Indexing Your Investments

Calculate the tax cost of switching. If you want to switch from an actively managed fund to a more passive index fund, you must first liquidate or sell off the assets you want to use, which typically triggers tax liability. Depending on how long you've invested in the fund and the type of account you have, you may also be assessed a penalty, which can be costly. In this case, it may be better for you to wait and switch several years down the road, when the cost will be less. Many financial advisors and wealth management firms have calculators that will figure out the tax cost for you – all you have to do is answer a few questions about your investments. If you spread out the tax cost over the projected life of your investment, you may find that it isn't cost-efficient to switch because the expense of switching eats up any benefit you would achieve through lower investment fees.

Research index fund costs carefully. While index funds have a reputation for lower fees than actively managed funds, some index funds have higher costs than others. While you won't be paying the management fees, there may be other costs. As many as 20 percent of index funds have higher costs than the average in their categories, so it pays to look not just at specific funds but also at others that are similar. When you look at fees on index funds, keep in mind that they may use different terminology than that with which you're familiar. While you can ask your broker or financial advisor to explain these to you, in general, the terminology doesn't matter. If it looks like a fee and is charged like a fee, it's a fee.

Meet with your financial advisor. If you've decided you want to switch all or part of your portfolio to index funds to lower your investment fees, your broker or financial advisor may have some recommendations for you. In some cases you won't have to move your investments to a different brokerage firm to invest in index funds, particularly if your broker works in a relatively large firm. However, keep in mind that your personal broker may not handle index funds. If you plan on keeping your assets with the same firm, your broker may be able to introduce you to a colleague who can handle your index funds, or advise you on other steps you'll need to take first.

Allocate your assets. When you invest in an index fund, all of that money is fully invested in that fund and you have no freedom to build up cash when the market is volatile or sinking. For this reason, it may be a good idea to keep a portion of your assets in an actively managed fund even though you'll pay higher investment fees. If the fees on your actively managed fund are especially high, you may want to divest some of the money in it (if possible), and keep your holdings there as low as possible. This will help lower your investment fees. Keep in mind that the larger the investment, the higher the fees. Investing in several different types of index funds is a good way to diversify and rebalance your portfolio so that your investments are more resistant to changes in the market.

Shopping Around

Talk to other investment services. If your investment fees are too high and negotiation didn't work, your best bet if you want to lower your investment fees is to find a different investment service with lower fees, or flat fees. If you have close friends or family members with similar investments to yours, you might ask them which broker or advisor they use and whether they're satisfied with those investment services. Don't choose an investment service based solely on its advertising or marketing materials. Instead, dig deeper by doing research online about the service's background and reputation, talk to past and current clients, and ultimately talk to someone who works there. Since you're considering moving your investments to lower your investment fees, make sure you understand all fees you'll be charged up front so you can compare and contrast the impact on your portfolio over time and make the right choice.

Consider tax consequences and fees for transferring accounts. If you have investment accounts with one broker and decide you want to move them elsewhere to lower your investment fees, there may be some cost in doing so. For example, you may need to sell off some investments if you want to transfer those funds to a different broker. Particularly in the case of certain types of retirement accounts, you may have to pay a substantial tax penalty for doing so. Your current broker also may charge a fee for closing out your account before a specified date, and those fees may be significant. If transferring your account will result in tax penalties and fees, those costs may offset any savings you would gain from lowering your investment fees.

Use FINRA to research brokers. If you're looking for a U.S. broker, you can look them up on the Financial Industry Regulatory Authority (FINRA) website. FINRA is a non-governmental, nonprofit organization that regulates investment and securities firms in the United States. You can access FINRA's "BrokerCheck" service at brokercheck.finra.org. The service is free of charge, and will provide you information about individual brokers as well as brokerage firms. Through this service, you can learn more about a broker's background and employment history, licensing, and whether they've had any regulatory actions or complaints against them.

Look for a fee-only advisor. A fee-only advisor can save you money because while they'll still charge you investment fees (and those fees may be the same or even more than what you're currently paying), you won't have to cover the advisor's commission. This will only save you money if your current broker or financial advisor is getting additional compensation or a commission for managing your investments. Keep in mind that fee-only advisors typically have a more passive management style, even if you're not investing in index funds. If you prefer an active management style, you may not be able to get what you want from a fee-only advisor.

Comments

0 comment